Execution and Risk Management

Why Profitable Mistakes Destroy Futures Traders: The Silent Killer of Consistency

"Consistent profitability in trading does not come from predicting the next tick. It comes from the unyielding quality of your decision-making process. The most dangerous trap a trader can fall into is the profitable mistake: a rule-breaking trade that makes money but systematically destroys compounding."

For futures and funded traders, the ultimate goal is consistency. You spend months studying price action, configuring indicators, designing trade models, and refining your pre-market routine. You set strict risk parameters and commit to following your playbook. Yet, many traders find themselves stuck in a frustrating cycle of passing evaluations only to blow their funded accounts days later.

When trying to diagnose these execution failures, traders usually focus on prediction accuracy or psychology. They search for a better technical setup, read motivational books, or blame a lack of raw willpower. However, this misses the root cause of systemic failure. The primary threat to a trading business is not a series of disciplined, structured losses. The true silent killer is the profitable mistake: a trade where you break your rules, ignore your playbook, execute impulsively, and make money anyway.

This article deconstructs the mechanics of profitable mistakes, details why they systematically destroy compounding, explains the player-versus-player (PVP) structure of lower timeframes, and outlines a practical, infrastructure-driven blueprint to align your execution with positive expected value.

1. The Illusion of Success: Systematic Losses vs. Profitable Mistakes

To operate a trading business professionally, you must understand that the outcome of a single trade is completely irrelevant. Because financial markets are probabilistic systems, any individual trade has a random distribution. A perfect, high-expectancy trade can result in an immediate stop-out, while a highly impulsive, rule-breaking trade can result in a massive financial windfall.

To build a compounding equity curve, you must separate trade outcomes from trade execution quality. This requires categorizing your trades into a quadrant of decision quality vs. financial outcome:

| Execution Quality | Winning Financial Outcome | Losing Financial Outcome |

|---|---|---|

| Rule-Compliant (Playbook) | Good Trade: Systematic Win. Positive expected value reinforced. | Good Trade: Systematic Loss. Cost of doing business under positive expected value. |

| Rule-Violating (Out of Playbook) | Profitable Mistake: Lucky but toxic. Reinforces negative expected value behaviors. | Bad Trade: Unsystematic Loss. Punishes rule-breaking behavior, but damages capital. |

A **Systematic Loss** is a trade that aligns perfectly with your playbook parameters but hits your stop-loss. It represents the cost of doing business. In a positive expected value model, a sequence of systematic losses is mathematically accounted for and easily recovered through normal variance. These losses are healthy and necessary.

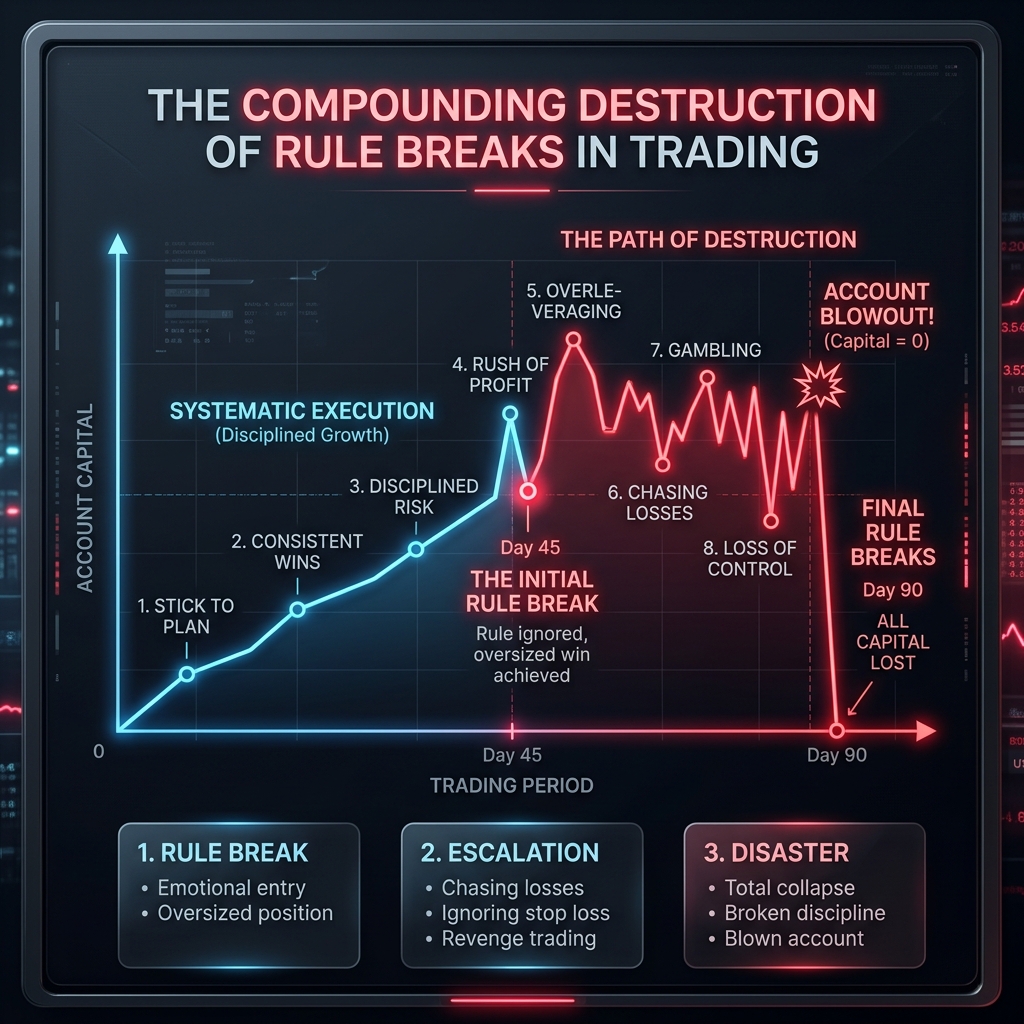

A **Profitable Mistake** occurs when you enter a trade out of fear of missing out (FOMO), chase a breakout, size up too heavily, or remove a stop-loss, and the market happenstance reverses to save you. Although your P&L displays a profit, this trade is a failure. You committed a operational error and were rewarded for it by short-term market noise.

Key Takeaway

Profitable mistakes teach your brain that bad behavior is rewarded. This reinforcement loop is the single greatest cause of eventual account blowout, as it encourages you to repeat high-risk behaviors with larger size.

2. The Neurological Trap: How Lucky Wins Destroy Compounding

The human brain is an efficiency machine designed to find patterns and seek instant reinforcement. When you perform an action and receive a positive reward, your brain releases dopamine, signaling that the behavior should be repeated. Under stress, your cognitive processing shifts from the logical prefrontal cortex to the primitive, emotional amygdala.

When you make a profitable mistake, your brain registers the positive financial outcome and connects it to the rule-violating behavior. It does not understand that the win was a random statistical variance. Instead, it codes the action (such as averaging down into a losing NQ long position) as a successful survival strategy. The next time you face a losing trade, your emotional brain will recall this experience and prompt you to repeat the error.

This creates a compounding destruction curve. You might get away with a profitable mistake once, twice, or even ten times. This success builds a false sense of security, encouraging you to increase your contract sizing. Eventually, the market moves into a sustained trend without a retracement. Because you have trained yourself to violate your stop-loss or average down, you execute the same mistake with heavy leverage, resulting in a single, catastrophic account blowout that wipes out weeks of disciplined work.

"Most traders fail not because they lack market opportunities, but because they treat luck as skill, reinforcing negative expected value habits until the market inevitably enforces the real statistics."

3. The PVP Arena: Lower Timeframes as Player-Versus-Player Environments

A common misconception among retail traders is that the market is a passive entity that slowly moves between technical levels. In reality, especially on intraday and lower timeframes, the market is a high-speed, zero-sum, Player-versus-Player (PVP) arena. You are not trading against charts: you are trading against other participants, high-frequency algorithms, and institutional desks.

On lower timeframes, technical setups (such as support levels, head-and-shoulders necklines, and channels) are self-fulfilling prophecies driven by participant positioning. If price approaches a major low, buyers are looking for support, while breakout sellers are placing sell-stop orders below the low. The institutional algorithms do not view this low as a line on a chart: they view it as a concentrated pool of liquidity (stop-losses) that can be swept to fill large buy orders.

To survive in this PVP environment, you must execute with absolute structural context. You cannot afford to guess or trade on gut instinct. You must identify where the large players are forced to act in their own self-interest. For instance, when a head-and-shoulders neckline breaks, the resulting move is fast because buyers are forced to cover their positions, and momentum sellers are jumping in. If you enter this environment without a strict playbook, you will be swept away by algorithms that exploit emotional retail positioning.

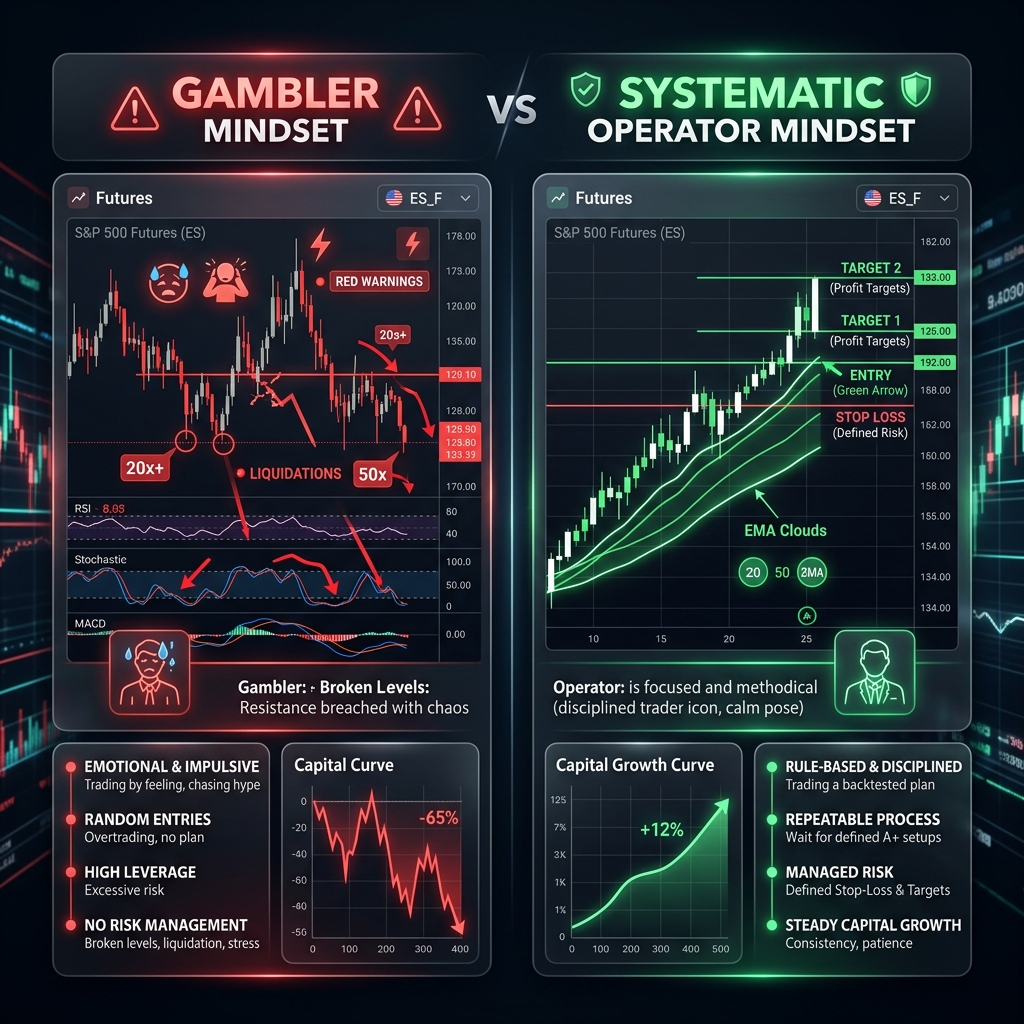

The Gambler's Reality

Treating the market as a random casino. Entering trades without a playbook, chasing volatility, ignoring daily risk limits, and believing that a string of lucky wins validates poor execution habits.

The Operator's Routine

Approaching trading as a quantitative business. Designing structured playbooks, executing with strict risk guardrails, logging execution deviation metrics, and treating a profitable mistake as a severe operational failure.

4. The Playbook Blueprint: The Catalyst-Setup-Trade Framework

A professional trader does not sit at the screen at 9:30 AM and look for generic patterns. They execute a predefined playbook. A playbook is a document that defines specific market scenarios, the participant behavior within those scenarios, and the exact rules for execution.

To build an effective playbook, you must structure your setups using the **Catalyst-Setup-Trade Framework**:

A. The Catalyst

The catalyst is the macro driver or market condition that generates the opportunity. It answers the question: *Why should this market move today?* Examples of catalysts include:

- A major macroeconomic news release (such as CPI, FOMC, or non-farm payrolls) that shifts interest rate expectations.

- An earnings release that creates an overnight price gap.

- A significant volume expansion indicating institutional rotation.

- A scheduled time-of-day volatility window (such as the New York open).

B. The Setup

The setup is the higher timeframe technical structure that defines the boundary lines of the trade. It answers the question: *Where is the high-probability zone?* Examples of setups include:

- A breakout of a five-day consolidation range.

- A pullback to the daily volume-weighted average price (VWAP) or prior day high.

- An overextension outside of a higher timeframe Bollinger Band.

- A clear market structure sequence of higher highs and higher lows.

C. The Trade

The trade is the lower timeframe execution trigger and order flow event that signals the entry. It answers the question: *When do I enter, and how do I manage the risk?* This involves reading the tape, identifying volume spikes, or waiting for a specific candlestick pattern to confirm the turn.

How To Apply This

Never execute a trade that lacks any of these three components. If you have a technical setup but no catalyst, you will likely get chopped up in a range. If you have a catalyst but no technical setup, you have no reference point to define your risk. Write down these three variables for every playbook strategy you trade.

5. The ASET Protocol: Grounding Your Execution in Structure

Once you have defined your playbook, you must systematize your trade execution. Human instinct prompts us to look at a chart, find a desirable entry point, and jump in, thinking about stops and sizing afterward. This reactive behavior leads to emotional execution. To eliminate this, you must follow the **ASET Protocol** sequentially for every position:

A - Allocation

Before you look at where to enter, you must determine your risk allocation. You must ground your risk in your account capital, not the chart. A professional model starts by defining your daily stop limit: for example, 2% of your total account equity. You then divide this daily stop limit into smaller slices (e.g., a buffer of several trades per day) to ensure a single trade cannot ruin your session.

S - Stop

Identify the exact price level where your playbook setup is invalidated *before* you calculate your entry. The stop-loss must be based on market structure (such as below a swing low or above an unbroken level), not an arbitrary dollar amount. Placing your stop first allows you to calculate your position sizing accurately based on your defined allocation.

E - Entry

Determine your entry trigger. You must decide whether your entry will be **predictive** (setting limit orders at key support or resistance levels) or **reactionary** (waiting for price to confirm a reversal, such as an engulfing bar or tape acceleration, before executing a market order). Reactionary entries are generally superior for newer traders as they provide real-time validation of the setup.

T - Target

Define your profit targets before entering the trade. A simple and effective method is to use **measured moves** based on standard deviations of the opening range or average true range (ATR) tick multiples. Standardizing your targets removes the temptation to exit early out of fear or hold too long out of greed, allowing the expectancy math of your system to function.

Recommended Tool

Managing these order parameters manually during fast market conditions is a major source of execution slippage. Nexus Chart Trader automates this process directly within NinjaTrader 8. By utilizing *Dynamic ATR-Based Take Profits* and *Previous Candle Stop Loss (Prev-SL)* trailing, the platform handles the execution mechanics, allowing you to focus strictly on structural analysis.

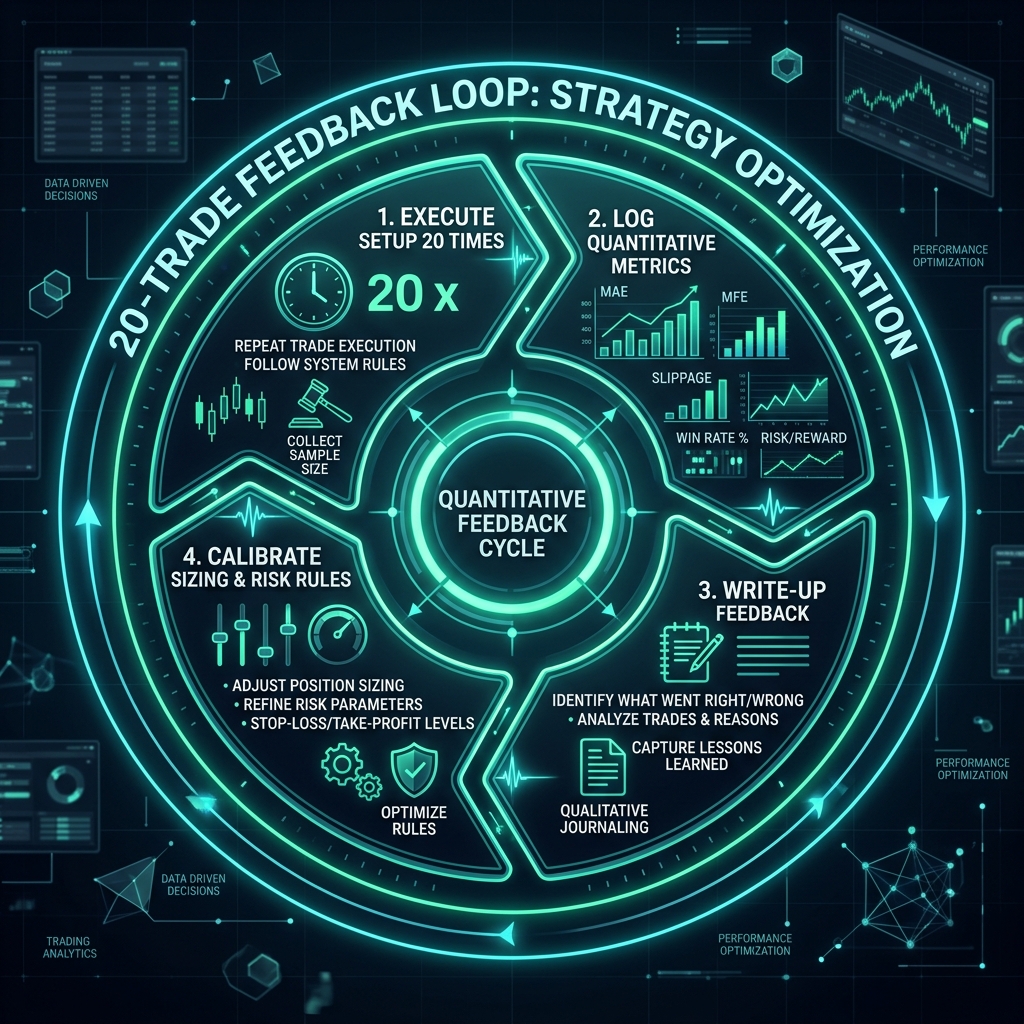

6. The 20-Trade Repetition Rule: Gathering Objective Performance Data

Traders often fall into the trap of constant strategy optimization. They take three trades with a new setup, suffer two losses, assume the strategy is broken, and change their indicators. This is an operational error. You cannot evaluate a probabilistic edge over a handful of reps.

To establish a valid statistical baseline, you must implement the **20-Trade Repetition Rule**:

- Define one trade setup with strict, unchanging parameters for your allocation, stop, entry, and target.

- Execute that setup exactly 20 times in the live market. You are not allowed to change your rules, size up, or skip valid setups during this trial.

- Write a detailed journal entry for every single trade.

Your trade write-up must focus on objective market feedback, rather than emotional reactions. Do not write "I felt frustrated" or "I got swept by algorithms." Instead, answer three structural questions:

- **What happened?** (Did the price hit the target, stop, or did the session end?)

- **Why did it happen?** (Did volume support the move? Did price react to a key VWAP band or market structure pivot?)

- **What is the feedback?** (Did the trade experience significant maximum adverse excursion? Did it offer a higher risk-to-reward ratio?)

Once you reach 20 reps, analyze the data. You will have a clear, objective picture of your strategy's expectancy and execution quality, separated from the noise of individual trade outcomes.

7. Accountability Systems: Daily Report Cards, Peer Dynamics, and Pack Hunting

In institutional trading environments, traders do not operate in a vacuum. They utilize structured accountability systems to eliminate behavioral errors. Retail traders can implement these same principles to professionalize their execution:

The Daily Report Card

At the end of every trading session, grade yourself on execution quality, not financial performance. Your grade must be binary:

• **Grade A:** You followed your playbook, respected your risk parameters, and executed your system perfectly. A day where you lost $500 but followed every rule is a Grade A.

• **Grade F:** You violated your playbook, chased trades, over-leveraged, or averaged down. A day where you made $2,000 but broke your rules is a Grade F.

Peer Challenges

Form a network with other systematic traders. Rather than sharing generic trade setups, create execution challenges. For example, challenge each other to achieve a 10-day streak of Grade A report cards. By shifting the social reward from P&L to execution quality, you reduce the psychological pressure to make money and increase the motivation to maintain discipline.

Pack Hunting

This is a term used on institutional desks to describe a scenario where multiple traders identify a massive, high-probability market opportunity (such as a significant macroeconomic catalyst breaking a key daily level) and coordinate their resources to attack the move. During normal range-bound chop, traders execute their unique, individual edges. But when a major macro event occurs, the entire desk focuses on the same objective. This allows them to capture large trends with institutional size while mitigating individual risk.

8. Execution Infrastructure: Moving Beyond Willpower with Software Guardrails

Willpower is a finite cognitive resource. Every decision you make, chart you analyze, and emotional response you suppress drains your willpower. Under market pressure, this reserve depletes, and your primitive brain takes over. If your risk management strategy relies on willpower, it is structurally flawed.

Professional traders do not rely on willpower. They build **infrastructure**. They design an execution environment that automates risk control and eliminates the opportunity to make emotional mistakes. If the software prevents you from committing an error, you do not need willpower to remain disciplined.

How To Apply This

Configure automated risk guardrails within your trading terminal. If you know you are prone to revenge trading, configure your terminal to enforce a mandatory loss cooldown period after a stopped-out position. If you struggle with overtrading during low-volume sessions, implement daily max loss locks that shut down the terminal for the day. Secure your execution environment at the software level, protecting your capital from your own human limitations.

Recommended Tool: Nexus Risk Infrastructure

To build a robust execution infrastructure, you need tools that convert systematic risk principles into automated platform controls. Nexus Indicator provides a suite of professional-grade tools for NinjaTrader 8 designed to support this workflow:

- Nexus Chart Trader: Enforces automated execution discipline. It features *Tamper-Proof Daily Risk Locks* that persist across NinjaTrader restarts, preventing revenge trading. The *Profit Protector System* automatically flattens positions if your profit drops below a configured threshold, and the *Global Loss Cooldown* locks execution for a set period after a loss. Additionally, the *News Lock* automatically flattens and locks trading before high-impact events by tracking the economic calendar.

- Nexus Trading Journal: A comprehensive local performance database that tracks your win rates, average risk-to-reward ratios, and maximum adverse excursion (MAE), allowing you to identify whether your losses are coming from strategy variance or execution errors.

- Nexus Copier (Free & Pro): Synchronizes your trades across up to 3 follower accounts (free version) or unlimited accounts (pro version), reducing the cognitive load of managing multiple funded accounts.

- Nexus Data Downloader: Fetches historical market data for deep backtesting and market replay sessions, helping you build statistical trust in your playbook to overcome execution hesitation.

Conclusion: Operating Like a Business Owner

The difference between a retail speculator and a professional trader is the management of operational risk. A speculator focuses on the P&L of the next trade and celebrates lucky wins. A business owner focuses on the integrity of the process, treats a profitable mistake as a major operational failure, and relies on automated infrastructure to manage risk.

By implementing the ASET Protocol, executing with strict playbooks, collecting data over 20-trade samples, and utilizing automated risk locks, you remove human emotion from the execution loop. Stop trying to control the market, and start controlling your infrastructure.

Secure Your Risk Infrastructure

Do not rely on willpower to manage your capital. Equip NinjaTrader 8 with automated risk guardrails, tamper-proof daily locks, and volatility-adjusted execution tools.

Get The Nexus Bundle NowValentin V.

Lead Quantitative Developer • Nexus Indicator • GitHub • LinkedIn

Valentin V. is the Lead Quantitative Developer at Nexus Indicator, specializing in developing high-precision tools and indicators for NinjaTrader 8. With over a decade of experience in C# and NinjaScript, he has helped hundreds of prop firm traders professionalize their execution workflows through technical discipline, systematic risk management, and automation.

Frequently Asked Questions

What is a profitable mistake in futures trading?

A profitable mistake is any trade that violates your predefined playbook or risk rules but results in a financial profit due to short-term market variance. These are highly dangerous because they reinforce destructive execution habits, leading to eventual account blowout.

How does the ASET Framework help enforce execution discipline?

The ASET Framework structures every trade into four mandatory sequential steps: Allocation (defining risk as a small portion of your daily stop limit), Stop (placing the stop-loss level before finding the entry), Entry (using a reactionary trigger based on real-time price confirmation), and Target (standardizing exits with measured moves to eliminate second-guessing).

Why is low timeframe trading described as a player-versus-player (PVP) environment?

Lower timeframes are dominated by active intraday participants, algorithms, and market makers competing directly for liquidity. In these environments, technical patterns are self-fulfilling prophecies driven by participant positioning and forced liquidations, requiring traders to execute with precise structural context.

How does the 20-Trade Repetition Rule build statistical trust?

The rule mandates executing a single, unmodified trade setup exactly 20 times before analyzing performance. This provides a statistically valid sample size that separates strategy variance from behavioral execution errors, shifting the focus from individual trade outcomes to systematic expectancy.

Why does reliance on mental stops fail during market volatility?

Willpower is a finite cognitive resource that depletes under stress. During high market volatility, emotional triggers bypass the logical prefrontal cortex, leading to hesitation, revenge trading, or moving stops. Automated risk guardrails, such as tamper-proof locks, are required to enforce discipline structurally.